Index Universal Life

Index Universal Life

IUL - Swiss Army Knife

Of Financial Products

Video Summary Notes

Comparing IUL to a Swiss Army Knife:

College Planning: The IUL can be used to save for a child's college education, with the flexibility to adapt to changing circumstances.

Home Purchases: IUL can be used to save for down payments on homes, providing a tax-advantaged way to fund such purchases.

Retirement Planning: IUL can serve as a powerful retirement planning tool. Contributions are made during working years, and during retirement, tax-free withdrawals can provide a reliable income stream.

Starting a Business: IUL's cash value can be used to fund a new business, offering a flexible source of capital without traditional loan processes.

Estate Planning: The death benefit of IUL can serve as a tax-efficient way to pass on assets to beneficiaries, providing financial support after the policyholder's passing.Long-Term Care and Critical Illness: IUL can provide funds for long-term care or critical illness needs, offering flexibility and avoiding the burden of traditional care funding methods.

IUL Training - Matt Smith

Video Summary Notes

Identifying Potential IUL Clients

Matt advises identifying potential clients who are concerned about taxes, Social Security, Medicare, and national debt. He also mentions considering people in tax-deferred plans or contributing beyond employer matches.

Best Types of Money

Matt explains the hierarchy of money types, prioritizing free money (employer matches) and tax-free money, followed by tax-deferred and taxed money.

Maximize Withdrawal Strategy

Matt discusses the advantages of IULs in allowing for greater income withdrawal (around 8-10%) compared to traditional retirement accounts (4% rule).

Self-Employed Individuals

Matt highlights the importance of offering IULs to self-employed individuals who often lack traditional retirement accounts.

Business Partnerships and IULs

Matt explains how key man policies and buy-sell agreements can effectively use IULs to address partnership and ownership scenarios.

College Funds and IULs

Matt mentions how IULs can help save for college expenses while providing permanent life insurance coverage.

Social Security and Tax-Free Income

Matt emphasizes creating a tax-free income stream through IULs to complement Social Security without affecting adjusted gross income.

Focus Areas for IUL Opportunities

Matt advises focusing on 401k contributions above the match and mortgage interest rate savings as key areas to target for IUL opportunities.

Why IUL?

Video Summary Notes

Sources of Retirement Income

401K, 403b, 457

Social Security

Pensions

Social Security accounts for 25-75% of retirement income. How do you make of up the difference?

Advantages of IUL over Qualified Plans

No Contribution Limits (401k and IRA have yearly contribution limits)

Tax Free Death Benefit

Tax Free Income

Why People buy IULs?

People who are looking for another source of retirement income

People who want to contribute more than what is allowed by their 401k or IRA contribution limits.

People who are concerned that taxes will be higher in the future and would rather pay tax now on the seed rather than on the harvest.

Tax-Free Death Benefit

Tax-Free Income

Tax Free Death Benefit from IUL vs. 401K

Example, 65 year old who dies of a heart attack and has $300,000 in a 401K. That $300,00 is going to be taxable when you die, so your beneficiary's will not actually get the full $300,000.

With an IUL the full $300,000 will go to your heirs and beneficiary's on an income tax free basis.

Tax Free Income from IUL vs. Taxable 401K

Let's say someone puts $100K into a 401k, and it has grown to 1 million dollars by the time you reach retirement.

Question to ask yourself.....

How much of the million dollars do you really own?

In your 401k, you haven't paid uncle Sam yet. Let's say you are in the 20-30% tax bracket, you would pay $200,000-$300,000 in taxes.

With an IUL, you are using after tax money. Let's say your IUL has grown to 1 million dollars when you reach retirement. You own the full 1 million dollars. You don't have to pay taxes because you used after tax dollars.

Would you rather pay a 20-30% tax now or maybe a much higher tax when older?

Would you rather pay tax on the seed (premiums you put into the policy) or the harvest (nest egg)? 🌱or 🌲

Who buys IUL?

Self employed who might not have access to 401K

Business owners

Doctors, MD's

High Income Earners who need to be able to contribute more than 401k or IRA allows.

High Income Earners who make too much money and can't contribute to a Roth IRA

Mutual Of Omaha IULE

Video Summary Notes

Mutual of Omaha's Index Universal Life Express product.

Simplified Underwriting

Issue Ages 18 to 75

Face Amounts:

Ages 18 to 50: $25,000 to $300,000

Ages 51 to 60: Up to $250,000

Ages 61 to 75: Maximum $150,000

Knockout questions similar to term life express.

MVR (Motor Vehicle Record) Check: Mandatory for ages 18 to 35Phone Interview: May be required for ages above 35, specifically for 51 to 60 and 61 to 75 with additional lab history checks.

Product Details

Non-guaranteed illustration rates, emphasizing that they are around 6.13% vs. Foresters Smart UL which is about 4.2%. This comparison suggests that the Mutual of Omaha product offers better potential returns.

Policy Changes:

Face amount increases are not allowed in year one of the policy.Premium adjustments can be made by contacting customer service.Additional premium payments can be made to increase cash value.

Benefits for Clients

Terminal Illness: If a client is diagnosed with a terminal illness with a life expectancy of 12 months or less, they can access a portion of the policy's face amount.

Critical Illness: The product covers approximately 12 different critical illnesses, and if a client is diagnosed with any of them, they can receive an advance from the policy's face amount.

Chronic Illness: If a client cannot perform at least two out of six daily living activities due to a chronic illness, they can also access money from the policy.

Cash Value Accumulation & Return Of Premium

Matt discusses the product's level premiums for 20 years, highlighting that this allows for a full return of premium within that time-frame if the client wishes to exit the policy.

Cash value accumulation is linked to the performance of the S&P 500, one of the top 500 stocks in the U.S., outperforming 96% of mutual funds.

Easy Solve

The "easy solve" feature in Mutual of Omaha's mobile software can solve the premium payment until age 100. This means the policy won't lapse as long as premiums are paid.

Recommendation for Use

Clients above the age of 60, and particularly those between the ages of 60 to 70.

How To Sel IULs Vs. 401K

Video Notes

401k Created 1978 (in use by 1980)

Advantages of 401K

Pre-tax contributions allow for purchase of more shares

If taxes are lower in retirement, then pre-tax decision is a good one

Often comes with employer match = free money

Disadvantages of 401k

You don't own your whole retirement portfolio

You only make money when you sell

Limited yearly contributions

Penalized if money taken out prior to 59.5

Tax rates may be higher when retiring

Triggers higher AGI (adjusted gross income) which will increase provisional income and higher taxation of Social Security Benefits

In event of death, funds pass with tax burden.

Invested funds CAN LOSE MONEY

Advantages of an IUL

Grows tax deferred and income is non-reportable (tax free)

Unlimited contributions

Not penalized if money taken out prior to 59.5

If tax rates are higher in retirement, you are thankful you paid with after-tax money

DOES NOT trigger higher AGI (Adjusted Gross Income) so it will not increase provisional income and won't cause higher taxation for Social Security Benefits

In event of death, funds pass TAX FREE

Invested funds CANNOT LOSE MONEY DUE TO NEGATIVE RETURNS

Disadvantages of an IUL

If payments are not kept up or structured correctly, policy could lapse.

No employer match or defined contribution plan with indexing

Longer time to realize benefits "longer runway"

Surrender penalty if you want to cancel

Client must be relatively healthy and young

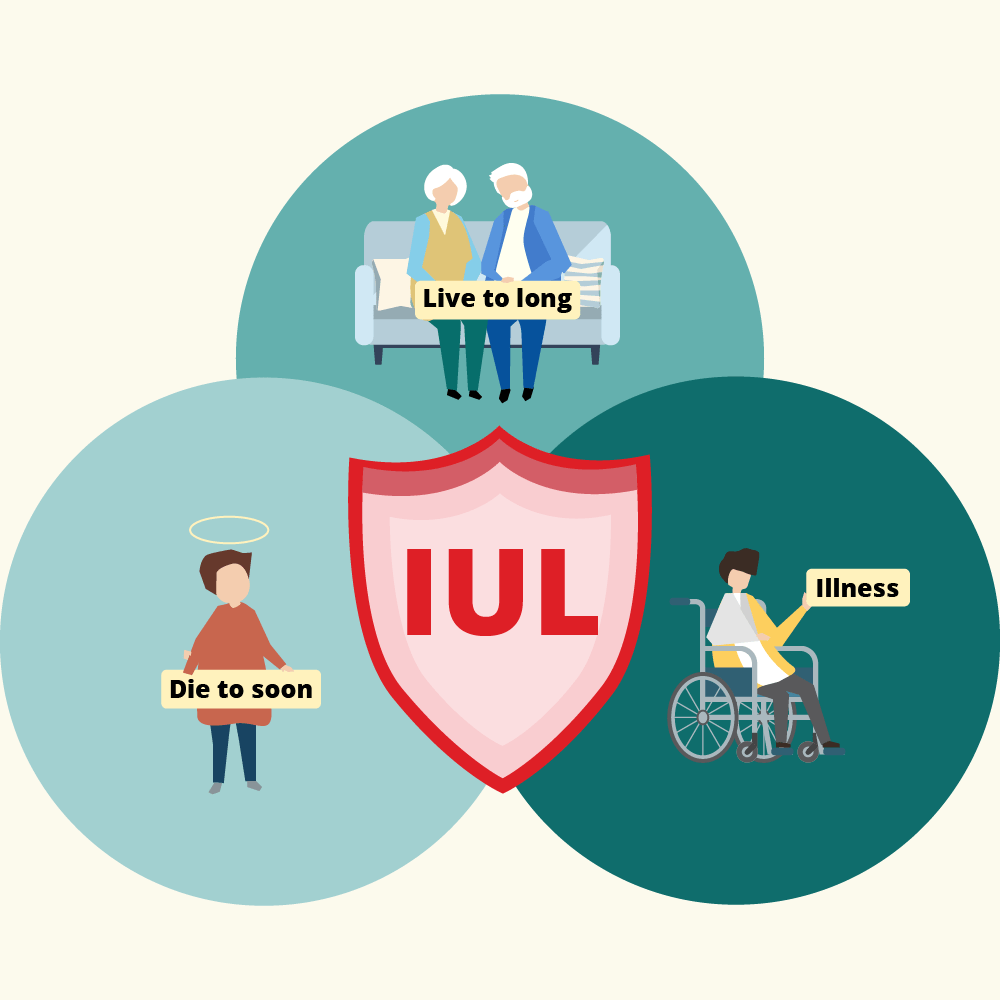

4 Reasons Every Agent Needs an IUL

#1 - Death Benefit

Video Notes

Reason 1: Tax Free Death Benefit

Limra Studies show the average person earning over $3 million in their lifetime.

Only 54% of adults have life insurance coverage.

Many agents lack sufficient life insurance coverage themselves.

Proposed Solution: Combine IUL with a Term Policy for comprehensive coverage.

Term policies are cost-effective and protect against unexpected early death.

#2 Tax Free Income

Video Notes

Reason 2: Tax-Free Retirement

Taxes are likely to go up due to the U.S. increasing debt

Avoid being taxed on your Social Security Income with IUL

IUL to create supplemental retirement

#3 - Long Term Care Alternative

Video Notes

Reason 3: Long Term Care Alternative

Long-Term Care Statistics: Statistics show the high likelihood (70%) of people needing some form of long-term care after reaching age 65. Traditional family-based care can be challenging due to financial constraints and a lack of planning.

20% will need long term care for more than 5 years

The Retirement Spending Smile: This term is introduced to explain how healthcare costs increase significantly in later years, especially towards the end of life. This underscores the importance of addressing potential long-term care expenses.

Accessing Living Benefits: Living Benefit allows you to access the death benefit early while you are still alive.

Critical and terminal illnesses trigger this benefit, providing a source of funds to address care needs.

Mutual Of Omaha IULE Illustration shown.

#4 - Estate Planning

Video Notes

Reason 4: Estate Planning

Avvo.com to set up a trust.

Life insurance is a way to transfer wealth in the most tax efficient way.

4 Plastic Cows Analogy: It's better to give up a little milk than to butcher two good cows. 🐄

For Fixed Index Annuity Training click below